Indian Economy Overview

Types of National Income:

Total value of all final goods and services produced with in country with in specific time period mostly one year is called National Income.

Measurement of National Income:-

- GDP

- GNP

- NNP

- NNPFc

- PI

- DP

GROSS DOMESTIC PRODUCT:-

Here income produced by resident citizens as well as foreign citizens who lives with in the boundary of country.

GDP = Q (Total quantity of G&S) x P (total price of G&S)

GROSS NATIONAL PRODUCT:-

Here income of all residents and nonresident citizens of country included but excluded income of foreigners who reside in the country.

GNP=GDP+(X(export)-M(import))

(X-M) is called Net factor abroad.

GNP = GDP+NFA

NET NATIONAL PRODUCT (NNP) :-

NNP = GNP – DEPRECIATION.

Depreciation means wear and tear of goods produced, depreciation reduced because of part of current product goes to replace the depreciated parts of goods already produced.

NNP (FACTORY COST):-

NNPfc = NNPmp-indirect taxes+ subsidy

Similarly

GDPfc = GDPmp-indirect taxes+subsidy.

Personal income:-

It is the sum of all income received by the entire people of the country in one year.

Personal income = National income + net transfer payments.

Disposable Income:-

Income available for a individual to spent on their own will.

Disposable Income = personal Income – Direct taxes.

National income at constant price and Current price:-

To compare the national income of various years it will be compared against one particular base year the price in this year is called constant price.

National Income at Constant Price = Total Quantity of Goods and Services Produced in a Particular Year multiplied by (The Price of Base Year).

National Income at Current Price = Total Quantity of Goods and Services Produced in a Particular Year multiplied by (Price of The Current Year).

GDP Deflator:-

It is the measure of level of prices of all domestically produced final goods and services, this is calculated to find overall rise in the level of price

GDP Deflator = Nominal GDP/Real GDP * 100

National Income Growth =

(National Income This Year – National Income Previous year)/National income Previous Year * 100

- National income at constant price shows negative growth.

- National income at current price shows positive growth.

Methods Of Measuring National Income:-

Players who participate to contribute to National income:-

- Individuals

- Households

- Business firms

- Foreign nationals.

The wage , rent ,interest are expenditure to business firms but income to households one’s expenditure is income to other and vice versa, so national income is calculated by compiling all expenditures of households this is called Income Method.

National income can be calculated by total values of goods and services produced this is called product method.

National income can be calculated by compiling all the expenditure incurred by people this is called expenditure method.

Product Method:-

Gross Value Added = Output of Final Goods and Services – Intermediate Consumption.

GDP = Gross Value Added + Indirect Taxes – Subsidy.

Income Method:-

GDP = Compensation of Employees + Consumption of Fixed Capital + (other taxes of production – subsidies of production) + Gross operating surplus

Consumption method or Expenditure Method:-

GDP = C (Expenditure of Consumers) + I (Expenditure of Investors) + G (expenditure of government)

Suitability Method:-

It says Product method is applicable for primary and secondary sectors and Income method for ternary sector.

Incremental capital output ratio (ICOR):-

It means additional capital required to produce one additional good.

ICOR = Incremental Capital/Incremental Output (Growth Rate).

IIP (Index of Industrial Production):-

It is measures growth of production in Mining, manufacturing and electricity industries; it will be released monthly by CSO

PMI (Purchasing Managers Index):-

Predicts the level of industrial production in advance.

Human Development (HDI):-

Human development is measured by three indices’ Health, Education, Standard of living, these three averages is considered as HDI (master index).

- The human development index was developed by Mahubub-ul-Huq along with Amartya Sen it is used by UNDP (United Nations Development Program).

- Every UNDP brings a Annual report call HDR(Human Development Report) , since year 1990,

- The method developed by them was followed till 2009 but from 2010 three new Indies’s added to HDI those are Gender Inequality index, Multi – dimensional Poverty index and inequality adjusted HDI.

Dimensions, Indicators and Goal Posts for Calculating HDI:-

HDI is measured in three Indies’s Health, Education, Standard of living

Indicators For these Indies’s:-

Calculation of HDI:-

Calculation method also underwent some changes in old Method and New method.

- Life Expectancy = it’s is same for both old and new methods.

- Education — in old method Adult literacy rate assigned to 2/3 weight and enrollment ratio assigned to 1/3 weight where both combined will add to 1. But in new method both the indices’ , Expected years pf schooling and average years of schooling are given same weight and their geometric mean is added to one, value will be in between 0 to 1.

Dimension Index = (Actual Value – Minimum Value) / (Max Value – Min Value).

- Income—- in old method it is calculated in log to the base 10 values the reason why it is used because beyond a certain range income does not enhance the human capability, so here Law of Diminishing Capability of Income ensured

- In new Method natural logarithm log to the base e used ( e=2.731) , there is no reason for using this but most of the income calculations use this log values. (Indian Economy)

- HDI is calculated as Arithmetic mean of index’s in old Method Now in New method it’s a Geometric Mean.

New Indices’:-

Multi Dimensional Poverty Index:-

It measures deprivation of people in health education and standard of living.

Inequality adjusted HDI (IHDI) :-

IHDI adjust the HDI for inequality in the distribution of dimensions – life expectancy, years of schooling and house hold income.

Gender Inequality Index (GII):-

It measures the inequality exists between men and women across the three indices.

Poverty and Unemployment:-

Poverty:-

Poverty is a phenomenon in which certain sections of people unable to fulfill their basic necessities of life. There are two types of poverty.

- Absolute Poverty

- Relative Poverty

- Absolute Poverty:-

In this poverty, minimum physical quantities like cereals, pulses, milk, butter etc are determined for subsistence level of living and their price quotations are obtained from market to convert these commodity requirements to money values.

By aggregating all the quantities included with money values a figure expressing per capita expenditure is determined .The population whose level of income below this per capita income is known as Below Poverty Line (BPL). This measure is also called Head count ratio. (Indian Economy)

Note:-

The reason why poverty is calculated based on consumer expenditure not on income because, senior citizens and children’s they will not earn but people can also consume more than their standard by borrowing also.

- Relative Poverty:-

In this case income/consumption distribution of population in different percentile groups estimated and a comparison of standard of living to top 5 to 10% people with bottom 5 to 10% people gives the relative standards of poverty, it is helpful to determine the inequalities in the society.

Quintile Income ratio = Average income of richest 20 %/Average income of poorest 20%

Estimation of Poverty in India:-

Dr. V M Dandekar and Nilkanth Rath, after independence poverty estimation is carried out by these two people in India.

- They fixed the minimum level of per capita nutrition for standard living is 2,250 calories and for rural the per capita income is 170 rs and for urban its 270 rupees as per 1960-61 prices

- Using these standards they stated that 177 million people were poor in 1960-61 and about 216 million were poor in 1968-69.

Planning commission expert Group report:-

- The planning commission appointed a expert group called Task force on minimum needs and effective consumption demand in 1989 as Dr. Lakdawal as chairman.

- Its submitted first report in 1993 it states per capita daily intake 2400 for Rural and 2100 for urban, precipitate is more for rural because of hard physical laborer they undergo.

- Different poverty lines are fixed in different states based on price variations and consumption of commodities across states.

- CPI-AL (Cost Price Index for Agricultural Laborer) is used for future update of rural poverty, similarly CPI-IW(CPI-Industrial Worker) and CPI-UNME (Urban non manual employee) for future urban poverty line.

61st Round of National Sample Survey Organization (NSSO) Survey and Poverty Examination:-

This round of survey is carried out during 2004-2005 , its is consumer expenditure survey , people are asked to remember and tell their 30 days expenditure and 365 days expenditure , from this data they have fixed the percapita as 365.30 rs and 538 rs for rural and urban respectively. (Indian Economy)

NSSO’s Mixed Recall Period (MRP):-

It involves estimation of poverty using consumer expenditure of 365 days recall period for 5 infrequently purchased non-food items like Clothes, Foot Wear, durable goods, Education and institutional Medical expenses.

Planning commissions Uniform Recall Period (URP):-

It involves estimation of poverty using consumer expenditure data of 30 days recall period for all items.

Tendulkar Committee on Poverty:-

- A committee named “Expert Group to Review Methodology For Estimation of Poverty” headed by D. Tendulkar was formed by planning commission in 2009.

- This committee adopted new method it moved calorie based poverty estimation to nutrition, health and other expenditure based estimation. It calls goods selected to estimate poverty as Poverty Line Basket(PLB).

- It relies on NSSO’s Mixed Recall Period, it calls to adopt urban poverty line for both urban and rural and it states consumption quantity is same for both just price will vary.

- As per this 446.68 rs rural poverty line and 578 rs urban property line. (Indian Economy)

Rangarajan Committee on Poverty:-

There was a lot of criticism for Tendulkar committee, so government appointed new committee as Rangarajan as head it used lode calorie based approach along with some other non essential food items to arrive at poverty line, as per this 972 rural per capita and 1181 for urban.

Ability of Pay Based Poverty Line:-

the author of this book argued in his article “Poverty Redefined” to fix poverty line at the level of Basic Exemption Limit(BEL) fixed for Income Tax purpose, the person whose income is below this is called BPL.

This is limit for an individual, suppose one person is earning in a family of 5 divide that by 5 and the output amount is the poverty Line.

Unemployment:-

Unemployment is a situation where people are willing to work at prevailing rate of wage but people could not get work.

Number of Unemployed = Labor Force – Work Force

Employment and Unemployment Estimates:-

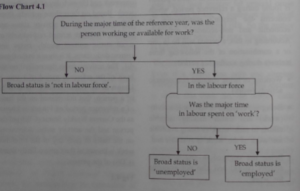

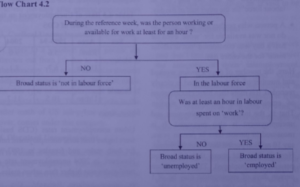

Activity Status:-

Employed: – Working or being engaged in economic activity.

Unemployed: – Being not engaged in any economic activity or making tangible efforts to seek work.

Not in Labor Force: – Being not engaged in any economic activity or not free for work.

Different Approaches to Determine Activity Status:-

Different Status is classified based on the activities pursued by them in some reference time periods. They are as follows.

- Usual Activity Status (US) — One year time period.

- Current Weekly Status (CWS) ==== each week period.

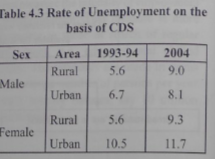

- Current Daily Status (CDS) === each day.

Usual or Principal Activity Status:-

Current weekly Status (CWS):-

Current Daily Status (CDS):-

- Here if a person is working 4 or more hours during a day he is termed as “employed”

- If a person has work for 1 hour or less than 4 hours is termed as ” employed for half day”, if anther half day he is seeking for work he is known as unemployed for the half day otherwise “not in labor force” for the half day

Types of Unemployment:-

- Structural Unemployment:-

It is caused by structural changes like rapidly growing population , changes in capital investments , technology change etc, its a long run in Indian Economy.

- Frictional Unemployment:-

It occurs when people change from one job to other and remain unemployed in the interval period; to avoid this people will resign the job after getting employed elsewhere.

- Cyclic Unemployment:-

It occurs when a employee thrown out of job due to a recession in economy, this is also called demand deficiency unemployment root cause of this unemployment is lack of demand.

- Disguised Unemployment:-

It is case where people are employed but their marginal product is zero, which means they are not adding productivity, this type of unemployment seen in Indian agriculture sector.

- Educated Unemployment:-

Even if a person is skilled and trained and failed to obtain a job as per his qualification is called educated unemployment.

- Open Unemployment:-

The labors live without any employment and don’t find any work to do is called open unemployment, it is seen when people migrated from rural to urban.

- Under Unemployment:-

It refers to under utilization of manpower in terms of both time and skill, for example when a post graduated work as a clerk or office boy it is called under unemployment.

- Voluntary Unemployment:-

Though the jobs are available people are not willing to work or rich enough or lazy.

- Natural Unemployment:-

Unemployment ranging from 2% to 3% in the country is known as natural unemployment, it can’t be eliminated at all.

Lorenz Curve:-

Lorenz curve maps the relationship between people and income.

in the above fig line AB is the line of equality

The line AEB is Lorenz curve, point E shows 90% people earn 60% of income remaining 10% earns remaining 40% this shows inequality.

Gini Coefficient:-

It measures inequality using lorzen curve

Gini Coefficient = Area above Lorenz curve/Area below Lorenz curve

Kuznets curve:-

It’s says in developing economy inequality increases in the beginning as the Indian Economy grows inequality decreases.

Engel’s law:-

PUBLIC FINANCE

BUDGET:-

Annual financial statement in case central article 112 and in case of state article 202 of the Indian constitution.

- Demand for grants is a statement estimated expenditure to be made out of consolidated fund of India, it require to be voted by Lok Sabha.

Budget will be calculated based on the following figures

- Actual figure of previous year

- Budget and revised figure for the current year

- Budget estimate for the upcoming year.

FUNDS:-

Funds are classified into three types.

- Consolidate Fund of India:-

According to article 266 (1) of constitution all revenues received by government of India and all loan raised by issue of treasury bills and all money from repayment of loans is known as “consolidated fund of India”.

- Public Accounts of India:-

According to article 266(2), funds which are not included in consolidated funds of India are called public accounts these mainly small scheme savings, PF schemes government is just of custodian of these funds it should be paid to in maturity or whenever the public claimed, these are called other liabilities.

- Contingency Fund of India:-

It is created by article 267 to meet unforeseen expenditure it is held at disposal of president of India.

RECEIPTS:-

Revenue: – Which need not to be repaid by the receiver.

Receipts = Revenue + Others

As article 112 and 202 of Indian constitution budget classifies receipts as below.

- Revenue Receipts:-

These are no need to be repaid by the government generally income from government assets. These are again classified as below.

- Tax Revenues:-

Revenue generated by levy and collection of Tax in India.

- Union excise duties :- Tax on production of commodities

- Custom duties:- Tax on Exports and Imports

- Corporate Tax:- Contribution of tax from the corporate sector.

- Income Tax: – Tax on personal income.

- Service Tax- Tax on services consumed by consumer.

- Taxes of Union territories: – Except Delhi and Pondicherry other UT tax is taken into central budget.

- Other Taxes and duties

- Non-Tax Revenues:-

- Interest Receipts: – Interest income from loans given by the central to state governments.

- Dividends and Profit: – Income from shares held by government in private and semi government enterprises.

- Other Non-Tax Receipts:-

i) Fiscal Services:

- Currency, Coinage, Mint :- Profit from the circulation of currency (Profit = Face Value – Manufacturing Cost)

- Other fiscal services: – Income Paid by RBI towards international obligations.

ii) Other General Services: – Income from Public Service Commission and central police.

iii) Economic Services: – Receipts from agriculture and allied activities.

iv) Social Services: – Receipts from department like education, sports, culture, and health.

V) Grants in Aid Contribution: – These are the receipts from forgein nationals and multilateral bodies as a gift.

- Capital receipts:-

- Receipts due to disposal of an permanent asset.

- Recovery of loans given to others

- Fresh loans raised by the government.

Capital Receipts are of Two types:-

- Debt Capital Receipts:-

- Borrowings

- Other liabilities

- Borrowings:-

Public debt or money raised on security of consolidated fund of India and repayable out of it. There are two types of borrowings.

- Internal Borrowings:-

Money borrowed with in the country from various sources.

i) Market Loans:-

Market loans are money raised by issuing bonds to the public and financial institutions.

Net Market Loan = Gross Market Loan – Repayment of Old Loans.

ii) Treasury Bills issued to RBI and other Banks:-

Treasury bills are securities issued by government treasury, these are zero interest bonds, they are issued at discount rate at the date of maturity redeemer will get total money they will be having different maturities.

iii) Other Internal Debt:-

Debt raised apart from two to meet the budget.

- Funded Securities:-

Sometimes short term treasury bills converted to market loans(long term) to defer the repayment these are called funded securities.

2. Other Special Securities Issued to RBI :-

Bonds issued outside of annual borrowing program like oil bonds, fertilizer bonds.

3. Ways and Means Advance:-

RBI acts as a banker to the government, it receives pay pays behalf of government if the balance goes to negative it lends short term loans to government this is called ways and means advance.

4. Special Floating Other Loans:-

Special loans schemes are launched to raise money, their interest revised periodically.

5. Securities Against Small Savings:-

Government of India created a fund in public accounts called National Saving Fund which bares P, insurance pension etc out of which 20% invested in central Government securities it is called security against small savings.

6. Securities Issued to International Financial Institutions:-

Securities issued to World Bank and other international organizations.

- External Borrowings:-

Money borrowed from the outside of the country.

- Multilateral Loans:-

These are loans received from IMF, World Bank etc , these are issued without any security.

2. Bilateral Loans:–

Loans raised from foreign governments and foreign government bodies directly.

- Other Liabilities:-

Liability means to repay these are the money government will use from Public Accounts of India for socio – economic development and has to repaid when claimed.

Small Saving scheme, Provident Funds , Other Accounts.

- Non-debt capital receipts:-

Amount received by government by the disposal of its assets.

i) Recovery of loans

ii) Disinvestment of government shares other than PSU’s.

National Investment Fund (NIF):-

Its is created for the disinvestment of PSUs, the funds of these are decided to be utilized for the following purpose.

- Subscribing to the shares issued by CPSE including PSB’s to make sure government 51% of ownership should not be diluted.

- Recapitalization of public sector banks and public sector insurance companies.

- Investment by government in RRB’s /NABARD, Uranium Corporation and Railways.

- Equity infusion in various metro projects.

Expenditures:-

- Revenue Expenditure

- Capital Expenditure

- Revenue Expenditure:-

Expenditure to meet day to day needs of governments that will not yield any future revenue is called revenue expenditure, these are one way payments.

Ex:- interest payments, defense , police, pension ,salaries, Grants to foreign governments, postal deficit etc.

- Capital Expenditures:-

Expenditure that creates permanent asset that gives income periodically.

Ex:- Loans given to state governments.

According to Article 34 of Audit Code expenditure is called capital based on below points.

- A productive asset may be considered as one which produces a sufficient revenue to afford a surplus overall charge to its functioning.

- The purpose of commutation of recurring liabilities is their extinction or reduction?

Deficit:-

Shortage.

- Budget Deficit =Total Expenditure – Total Receipts

= {(Capital Expenditure + Revenue Expenditure) – (Capital receipts + Revenue receipts)}

= {(Capital Expenditure + Revenue Expenditure) – (Borrowings + Other Liabilities + Revenue Receipts)}

- Revenue Deficit = (Current Revenue Expenditure – Current Revenue Capital)

- Fiscal Deficit = Budget Deficit + Borrowings fro RBI+ Other Liabilities.

- Primary Deficit = Fiscal Deficit – Interest Payments

- Monetized Deficit = Borrowing from RBI + Draw Down Balance of Government from RBI.

Types of Budget:-

- Performance and Programme Budget:-

In these budget chosen programs subjected to test of actual program against expected results, it involves stage wise planning. (Indian Economy)

- Outcome Budget:-

It is the compilation or anticipated and intended outcomes of various ministries; here outcome means benefits arise due to physical output from respective financial input.

- Zero based Budget:-

It involves a consideration there is no budget or scheme which needs to be started from scratch.

TAX:-

Tax is a compulsory levy payable by an economic unit to the government without any corresponding entitlement to receive a definite and direct quid pro quo from government.

Broad Areas of Tax:-

Tax on income and expenditure, Tax on commodities, tax on property and property transaction.

Tax Base:-

Legal description of object w.r.t which tax is payable.

Ex:- personal income is base for income tax.

Tax Buoyancy:-

Tax Buoyancy = Proportionate Change in Tax Revenue / Proportionate Change in GDP

= %TAX/%GDP

Tax Elasticity = Proportionate Change in Adjusted Tax Revenue / Proportionate Change in GDP

Classification of Taxation:-

Proportional Taxation: – Tax levied on a% of tax base irrespective of size of tax base at a uniform rate.

Progressive Taxation:- If tax increases with increase of tax base.

Regressive Taxation:- If tax decreases with increase in tax base.

Incidence of Tax:- It is the final resting place where tax payment can’t be avoided.

Ex:- Employee on Salary, Consumer on Goods.

Impact of Tax:– First point of contact with tax payers.

Ex:- Seller he can pay or pass on to consumer.

Methods of Taxation on Goods:-

- Ad Valor Em:-

If tax levied of % of the value of good irrespective of how many units produced/sold/imposed.

- Specific Duty:- If tax levied on flat rate per unit of good produced/sold/imported.

Types of Taxes:-

- Direct Tax:- Where incidence and impact lie with the same point

Ex:- Income tax , corporate tax, wealth tax ,Security Transaction Tax (SST), Commodity Transaction Tax.

Minimum Alternate Tax:- It is the tax imposed on companies which escape corporate tax with certain means , these are called zero tax companies , to make such companies to pay tax minimum 30% on profits is charged.

- Indirect Tax:- Incidence at one point and impact is at some other point.

Ex:- Custom Duties, Excise Duties

Sales Tax or Value added Tax (VAT):-

It is the tax on sale of commodities, it is imposed as a % of value added.

Central Sales Tax:- It is imposed by central and collected by state Government.

Service Tax:- Tax on service providers as well as consumers.

Goods and Services Tax (GST):-

It is the uniform Tax throughout the country; it has VAT features as well it is imposed on both goods and services.

Fiscal Responsibility and Budget Management Act (FRBM Act 2003):-

Act is enacted in 2003 with the purpose of correcting the fiscal imbalances like high revenue and fiscal deficit. Special features.

ACT:-

- Central to take appropriate steps to reduce fiscal deficit and revenue deficit.

- Central government shall not borrow from RBI except by way of advances to meet temporary excess of cash disbursement over cash receipts. (Indian Economy)

- RBI not to subscribe primary issues of central government.

- Central government has to take measures to maintain transparency in fiscal operations, they are

- Macroeconomic Frame Work:-

It contains assessment regarding GDP growth rate, fiscal balance of central government.

- Fiscal Policy Strategy Statement:-

Statement explains how current policies are in conformity with sound fiscal management principals and notifies for any major deviations.

- Mid -Term Fiscal Policy Statement:-

It set out three year rolling targets for four special fiscal indicators in relation to GDP at MP.

- Revenue Deficit

- Fiscal Deficit

- Tax to GDP Ration and

- Total outstanding debt at the end of the year.

Tax Regimes of Center and State:-

Center Tax List:-

Tax on income ( except agriculture), corporate tax, custom duties, Excise duties (except alcoholic beverages), Estate and succession duties ( other than agriculture), Rates of revenue stamps, Taxes on sale and purchase of news papers and advertisements etc, tax on railway fares and freight, tax on goods and passengers carried by road, air, sea, tax on interstate trade.

State tax List:-

All taxes on agriculture, land revenue, tax on goods and services except news papers, on land and buildings, excise duties especially on alcohol, all luxuries, Tolls, inland water trade, on advertisement other than news paper.

Tax Sharing Mechanism:-

Finance commission and parliament are the two institutions for tax sharing, states demanded share in corporate tax so, 80th and 88th amendments made. (Indian Economy)

After 80th Amendment 2000:-

Article 270:-

All taxes and duties referred in union list except taxes come under article 268, article 269, surcharge and cess.

Article 268:-

Stamp duties and excise duties imposed by center and collected by state.

Article 269:-

Interstate sale and purchase and Interstate consignment these are imposed and collected by states.

Article 252:-

Under this act any tax coming under state domain can be handed over to parliament this is called Rental arrangement.

After 88th Amendment:-

Article 268 (A):-

Service Tax is introduced, imposed and collected by central but shared.

Cess:-

It is a tax additionally levied as a percentage of existing tax amount for specific purpose.

Ex:- Education cess of 3% levied on all central taxes. (Indian Economy)

Surcharge:-

It’s also like cess but without any purpose.

Countervailing Duty:-

To counter balance subsidized imports the importing countries import duty to offset list lower price it’s called countervailing Duty.

Anti-Dumping Duty:-

Exporting goods to other countries in larger quantities is called dumping

- Price Dumping:-

Selling goods in foreign countries at a price lower than home country.

- Cost Dumping:-

Selling goods in foreign countries at a price lower than cost of production is also called predatory dumping.

Laffer Curve:-

Relationship between tax revenue and tax rate.

Tax revenue will be high at optimal tax value.

Off budget Liabilities:-

These are money liable to be paid by government to other entities as policy matters.

Ex:- Oil Marketing Enterprise(OME’s) bonds.

Fiscal Slippage:- A situation where fiscal deficit more than expected.

Fiscal Consolidation:- Long term permanent strategies to reduce expenditure to eliminate deficit.

Indian Financial System:-

Money Markets:-

Market for lending and borrowing of short term funds say up to 3 years.

Ex:- Commercial Banks, RRBs etc

Capital Markets:-

Market for lending and borrowing medium and long term funds more than 3 years.

Reserve Bank of India and Its Functions:-

It is the apex regulatory body of Indian banking system it keeps all cash reserves of all scheduled banks, hence known as “Reserve bank of India”.

- It was established in 1935 under RBI Act 1934 and its been nationalized in 1949 (Indian Economy)

Functions of RBI:-

To regulate issue of banks notes and keeping reserves with a view to keep monetary stability in India and generally to operate currency and credit system of India to its advantage.

Monetary Functions:-

Functions which are concerned duly with money.

- Bank of Issue:-

- Issue of money is an exclusive right of RBI except 1 rupee coins and notes (these are issued by ministry of finance).

- To issue money RBI keeps 115 cr in gold and 8 cr in foreign currencies as back up, this is called Minimum reserve system.

- Based on prevailing economic conditions, the need of economy RBI issues new money it should not lead to inflation.

- Banker and Debt Manager to Government:-

RBI acts as a banker to governments both center and state (except Sikkim and J&K).

- Bankers Bank:-

- RBI is the banker of all banks; it keeps the cash reserves of all banks in the form Cash Reserve Ratio (CRR).

- It is the lender of last resort; it manages money flow in the market.

- Custodian and Manager of foreign exchange.

- Controller of Credit:-

Credit control means control of lending and deposit creating capacity of banks, it result in control of money supply which controls inflation and promote economic growth.

Quantitative Method:-

These will aim at controlling the cost and quantity of credit, there is no discrimination between different sectors.

Conventional Measures:-

- Bank Rate Policy:-It is the re discount rate fixed by RBI for the first class bills and government securities held by commercial banks.

Bill of Exchange:-

Written document that assure payment of money to the seller by the purchaser at a future date.

Discount:-

If seller needs immediate money bank will redeem the bill by charging some amount of interest, bank will get full money at the date of maturity.

Re Discount:- The bank can redeem the bill at RBI at a interest rate less than it has given to seller before maturity, it’s called re discount.

By varying bank rate RBI controls credit, it is inversely proportional to profit.

- Open Market Operations:-

RBI sells financial instruments like bonds, securities, bills to the banks and public against their money, reverse also it will do, because of this money flow will increase.

- Variable Reserve Ratio:-

Cash Reserve Ratio:- Scheduled banks has to keep some amount of their Net time and demand deposit with RBI as security under RBI act 1934.

CRR = Cash Reserve/ Net time and Demand deposits * 100 (it will be b/w 3 to 15%)

Statutory Liquidity Ratio:- Scheduled banks has to keep some amount of their demand deposits in their vault itself. (Ratio will be 25- 40%)

Non-Conventional Measures:-

Liquid Adjustment Facility (LAF):- It has two instruments

- Repo Rate:-

The rate at which commercial banks borrow from RBI my mortgaging their dated government securities and Treasury bills.

- Reverse Repo Rate:-

The rate at which RBI borrows from commercial banks by mortgaging their its government securities and Treasury bills.

Marginal Standing Facility:-

It is the loan facility given by RBI to the banks which has SGL (subsidiary general Ledger) account with RBI, it’s a overnight loan (loan will be 1% of NDTL) minimum amount should be 1 corer.

Market Stabilization Scheme:-

It is a facility to control liquidity due to excess foreign exchange flow into country; RBI absorbs excess flow by issuing government securities.

Qualitative Credit Control:-

These methods discriminate between sectors; they control credit flow into particular sector or particular end use.

- Regulation of margin requirements:-

Margin is the amount contributed by borrower towards his borrowing purpose, by varying this margin for different sectors RBI will control credit.

Ex:- Two wheeler loan (deposit+ loan).

- Regulation of Consumer Credit:-

Consumer credit refers to credit to consumer to purchase durable goods in installments.

- Minimum down Payment

- period of repayment.

3. Rationing of Credit:-

In this method max amount flow into particular sector is controlled.

- Variable Portfolio Ceiling:-Max amount of credit is fixed for different sectors and different portfolios

- Variable Capital – Risk Weighted Asset Ratio:- CRAR = Capital/ Risk weighted Assets * 100

- Direct Action:- RBI will scrutinize loans of schedule banks.

Moral suasion, publicity.

Non Monetary functions: – Supervision, Promotional functions.

Composition o Money Market:-

Organized Sector:-

It consists of both banking sector and sub markets, banks will take both deposit taking and lending operations, sub markets will generate capital for banking sector

Banking Sector:-

It consist of commercial banks, RRB ‘s, Cooperative banks.

Public Sector Banks:-

Which has maximum ownership with government.

State Bank Group:-

Previous name of SBI is Imperial bank it was created in 1921, it was nationalized in 1959.

Nationalization done in two stages:-

- In 1969 banks whose reserves more than 50cr are nationalized.

- In 1980 banks whose reserves more than 200cr are nationalized.

Total public sector banks are 26

Private Sector Banks:-

Indian Banks + Foreign Banks

Indian Banks:-

Old Banks:-

The private banks set up before 1990.

New Bank:- Banks which are setup after 1990.

Local Area Banks (LAB’s):-

- They operate in minimum area; they can be set up maximum in 3 districts.

- They are registered under companies act 1956 with minimum capital of 5 cr.

Foreign banks:-

After 1991 reforms India opened doors for foreign banks.

Ex:- citi.

Classification of Banks:-

1). Scheduled Banks:-

- Banks which are listed in 2nd schedule of RBI Act 1934 , bank has to fulfill following conditions to come into this list.

- Minimum paid up capital and collected funds must be 5 lakhs.

- Any activity of bank should not affect the interest of depositors.

- They can avail loans and re discount facility from RBI.

2). Non-Scheduled Banks:-

Which are not listed in 2nd schedule, they have only CRR in RBI.

The Regional Rural Banks (RRB’s):-

Banks are established in1975, under RRB’s act 1976

- Public Sector bank will set up RRB’s, these are called sponsor of RRB.

- Total 196 banks setup.

Co-operative Banks:-

- These will have co operation of stake holders as motive.

- Certain group of people come together can establish a cooperative bank.

- “One Vote one person” principal.

- NABARD is the apex boby of these banks.

Composition of Cooperative Banks:-

Composition of Sub Market:-

Call Money market: – these are short notice loans, period ranging from 10 to 14 days, it’s a inter bank borrowing, rate at which they borrow is called call money rate.

Bill Market or Discount Market: – These are usually short term lending up to 90 days.

A). Commercial Bill market: – Bills issued to industrial traders. (Indian Economy)

B). Treasury bill: – These are securities issued by government, these are zero interest bonds, these are issued at discount rate.

i) Ad hoc Treasury bill: – it was issued for a particular end or case in hand, these are 91 days bill

ii) Regular Treasury bill: – these are regular bills issued to meet budget expenditure, these will have different maturities.

Certificate of Deposit: – these are issued by commercial banks and FIs; amount will be multiples of 25 L minimum 1 crore, maturity 3 months to 1 year in bank in FI 1 to 3 years.

Commercial Papers:- introduces in 1990 , min amount 1 crore denomination of 5 L, issued by FI and corporate PD’s.

Unorganized Sector:-

There is no systematic procedure. 1) Money Lenders, 2) Merchant cum money lender.

Banking Schemes:-

Lead Bank Scheme: – Any one public sector bank will be selected as lead bank of the district, it will supervise all bank functions ensures that same person will not get loan from two banks.

Differential Rate of Interest: – Every year bank has to give 1% of its total deposits as loan to weaker section people, in this 40% should be SC/ST.

Social Banking: – Financing poverty reduction and employment program of government is called social banking

Priority Sector Lending:-

- Priority sectors are sectors which contribute to national income but will not get loan from commercial bank.

- A target of 40% of Adjusted Net Bank Credit(ANBC) or credit equivalent amount of off Balance Sheet Exposures(OBE) whichever is higher is stipulated for lending of priority sector by banks.

- 18% for agriculture —->13.5% direct Lending and 4.5%

- priority sector lending for RRB’s is 60%

- Short falls in priority sector must be deposited in NABARD infrastructure development fund; NABARD will give it to state Govt development activities.

- ANBC = Credit outstanding at the end of Financial year – credit outstanding at the beginning of financial year.

- Off balance sheet exposure: – Example: – Bank guarantee a loan by someone from some other FI, actually this is not a liability of bank, if person fails to repay then it will become.

Financial Inclusion: – Means including people to financial system, for this RBI introduced “No Frill accounts”(zero balance)

Capital Markets:-

Non Banking Financial Corporation (NBFC):- It is established under companies’ act 1956 and engaged in business of loans and advances.

Difference between NBFC and Banks:-

- NBFC will accept deposits but not Demand Deposits.

- NBFC can’t issue cheques.

- Bank deposits will have insurance NBFC don’t have.

Composition and Functions of Capital Market:-

Security Markets:-

- They deal with Shares and Debt instruments.

- Shares—-> (equity shares, preference shares, derivatives etc.)

- Debt Instruments—-> (bonds ,debentures etc)

- Both are used for fund raising but main difference is in shares investors will have profit in both capital and profit.

- In case of debt investors receive only interest but company has to pay interest regardless of profit or loss.

Debenture: – These are bonds with some security usually some plant machinery etc.

Equity Shares:- Shares has claim on overall capital profit or loss.

Preference shares:- They are entitled to have a fixed amount of interest and they are entitled to get back paid capital as bonds.

1) Government Securities Market: – These are markets for government and semi government securities backed by RBI.

2) Industrial Securities Market: – For industries.

New and Old issue Markets:-

New Issue Market: – Sell and purchase of new securities carried out.

Old Issue market:-sale and purchase of securities those are already issued in new market.

Securities and Exchange Board of India (SEBI):- Established in 1988 and got statutory status in 1992, head office Mumbai. (Indian Economy)

New Issue Market:-

Public Issues: – Issue of securities to public.

- IPO —> if a company issuing shares for the first time it is called Initial Public Offering

- FPO —> if an existing company issuing to raise funds it’s called Follow on Public Offering

Issue Process: – 2 types in new market

- Declared price Issue: – Already share price is pre fixed.

- Book Building: – First company will see no of applications then price will be decided.

- Merchant Banker: – Bank which do fund raising behalf of company.

- Authorized Capital:– Max money authorized by Memorandum of Association (MOA) of a company that can be raised by company.

- Issued capital: – Actual amount of securities issued.

- Subscribed Capital: – Amount of securities sold.

- Underwriter: – Financial firm who agreed to buy unsold securities.

- Called up Capital: – Money paid from subscriber.

- Paid up Capital: – Money paid to subscriber.

Other Issues: – Issued to only a closed group of people.

Private Placement: – Offering securities directly to high volume worth investors.

Right to Issue: – Offer of security to existing share holder in the FPO.

Bonus Issue:- Offer of shares against distributable profit to existing share holders.

Sweat Equity Issue:-

- Offering shares to the employees against their labor.

- Employee Stock Offer Scheme (ESOS) —-> in this scheme employees offered shares at a future date at a predetermined price.

- Employee Stock Purchase Scheme (ESPS) —->only employees offered shares as part of public issue, money will be deducted from salary between issue date and purchase date.

Old Issue Market:-

Stock Exchange: – Institution for buying and selling of listed securities.

Over the Counter Exchange:- Platform for selling the securities those are not listed in a stock exchange.

Trading Process:-

Brokers:- Registered member of stock exchange to trade on behalf of client.

Cash Trading: – Buying selling takes place at the prevailing price of the trading day.

Forward Trading: – Buyer and seller agree to trade at a future date at a predetermined price irrespective of price on the trade day.

Futures: – In case of this both buyers and sellers has to execute the agreement.

Options:- In this case buyer or seller can withdraw for this they have to forgo the deposited premium amount, for seller it’s called Put option, for buyer it’s called Call Option.

Stock Exchanges:-

National Stock Exchange: – Established in 1993, IDBI is the main promoter of NSE.

Bombay Stock Exchange: – Established in 1887, previously owned by stock brokers now its demutualised (means transferring from brokers to public).

Index:-

Indices in India are sensex , Nifty , Nifty Junior.

Sensex (Sensitivity Index):- This is the index of Bombay Stock Exchange , it’s the price movement of top 30 companies (blue chip companies).

Nifty (National Index for Fity):- This is the price movement of top 50 companies.

Nifty Junior: – Price movement of next 50 companies.

Free Float Market Capitalization: –

Value of traded share (Value of Traded Shares = No of Shares * Price of Each Share)

Market Capitalization: –

Value of traded + Non traded shares.

Depositories:-

Institution that keeps securities in electronic format.

Two Depositories 1) National Securities Depository Limited (NSDL) by NSE and IDBI

2) Central Depository Services India Ltd (CDSL) by BSE.

Clearing Houses: –

Enabling easy settlement of security trade, like depositories help in change of ownership and delivery of security.

Clearing Banks: –

Mediate the fund transfer between buyers and sellers Ex: – NSCCL (National securities Clearing Corporation).

Rolling Settlement: –

It is represented as T+2 (T is trade day) +2 is days means 2 working days for the settlement of trade.

Development Financial Institutions:-

Which provide long term loans (more than 25y) and entrepreneurial assistance to industries Ex:- IDBI

Financial Intermediaries:-

Capital market institutions other than stock exchange, classified as below.

RBI Regulated NBFCs:-

These are classified as below.

1). Equipment leasing Company:-

They own machineries and give them on lease for rental income.

2). Hire – Purchase Company:-

Companies which finance installment purchase.

From 6th dec 2006 NBFC’s reclassified as

1). Asset Finance Company:-

Company which finances a physical asset which carries productive economic activity.(Ex:- Vehicle finance).

2). Loan Company:-

They provide car loans and mortgage loans

3). Investment Company:-

Which invest in Shares.

SEBI Regulated NBFCs:-

1) Venture Capital Companies:- These are the companies which provide finance to new products based on innovation.

2) Merchant Banks:- Provide consultancy and corporate advisory services to corporate clients for raising funds and other financial aspects.

3) Stock Brooking company:- Recognized by SEBI for mediating stock exchange.

NHB Regulated NBFC:- Housing loan companies finance purchase and construction.

Nidhi Companies are regulated by Department of Company affairs(DCA) and RBI.

Face Value :- Actual value of share

Share Price:- Actual value + share premium

Short Selling :- Selling securities without buying (by Borrowing).

Bull and Bear Trading:- Bull trading buyers buys more shares with the intention of profit in future, Bear trading buyer will be buy less to avoid loss in future.

Secularization:- Converting existing assets to securities , bank will sell NPAs to Asset Reconstruction companies(ARCs) they will divide and sell to investors.

Buy back :-

Issuer buying the shares again to accumulate shares in his hand.

Market Capitalization – GDP ratio:- Total Market Capitalization / GDP

Price Earning Ratio = Price per share/Earning per share

Net Asset Value = Total Asset value – liabilities

Transferable Securities:-

We can change ownership of these securities , Vice versa for non transferable.

Cumulative and Non – cumulative:-

Securities entitled to receive dividend of particular year in coming years as a arrears is called cumulative , non cumulative don’t have this right.

Convertible and Non convertible securities :-

One type of securities are converted to other type (Ex bond to shares).

Mutual Funds:-

Mutual funds help investors, it will mobilies public savings and invest in securities.

Hedge Funds:-

Its similar to mutual funds but in this case not public funds a hand full of investors join to form fund.

Commodity Exchange:-

A platform to sell and buy agricultural products and natural resources like iron , crude oil etc.

Money Stock Measures:-

Money stock means total amount of money available in economy at particular point of time.

- RBI the monetary authority of India was publishing money statistics from July 1935. (Indian Economy)

- It has changed the methodologies three times depend on the committees formed.

- Now we are using third recommendation in which Liberalization , privatization, Globalization reforms are considered.

Money:-

“Set of liquid Financial assets , the variation of stock it could impact aggregate economic activity”

Sectorization of Economy:-

Monetary and Liquid aggregates:-

Third committee recommendations:-

It recommended compilation of four monetary aggregates on the basis of balance sheet of bank in conformity with the norms of progressive liquidity

M0-monetray base, M1-narrow money M-2 and M-3 Broad Money in addition to these group also recommended compilation of three Liquidity aggregates.

Reserve Money(M0) =

Currency in circulation + Bankers Deposit with RBI + other deposits with RBI

Narrow Money (M1) =

Currency with public + Demand deposits with banking system + other deposits with RBI

M2 = M1 + Savings Deposits of Post-Office savings bank

Broad Money(M3) =

M1 + Time Deposits with banking system.

M4 = M3 +All deposits with Post office Savings bank( excluding national saving certificate).

NM1 = currency with public + Demand Deposits with banking system +other deposits with RBI

NM2 =NM1+Short term time deposits of residents(including contractual maturity of one year)

NM3 = NM2 + Long term deposits of residents +Term funding from financial institutions

L1 = NM3+ All deposits with the post office savings banks.

L2 = L1 + Term deposits with term lending institutions and FIs + Term borrowing by FIs + Certificate of Deposit issued by FIs

L3 = L2+ Public deposits of non banking Financial companies

Inflation and Deflation:-